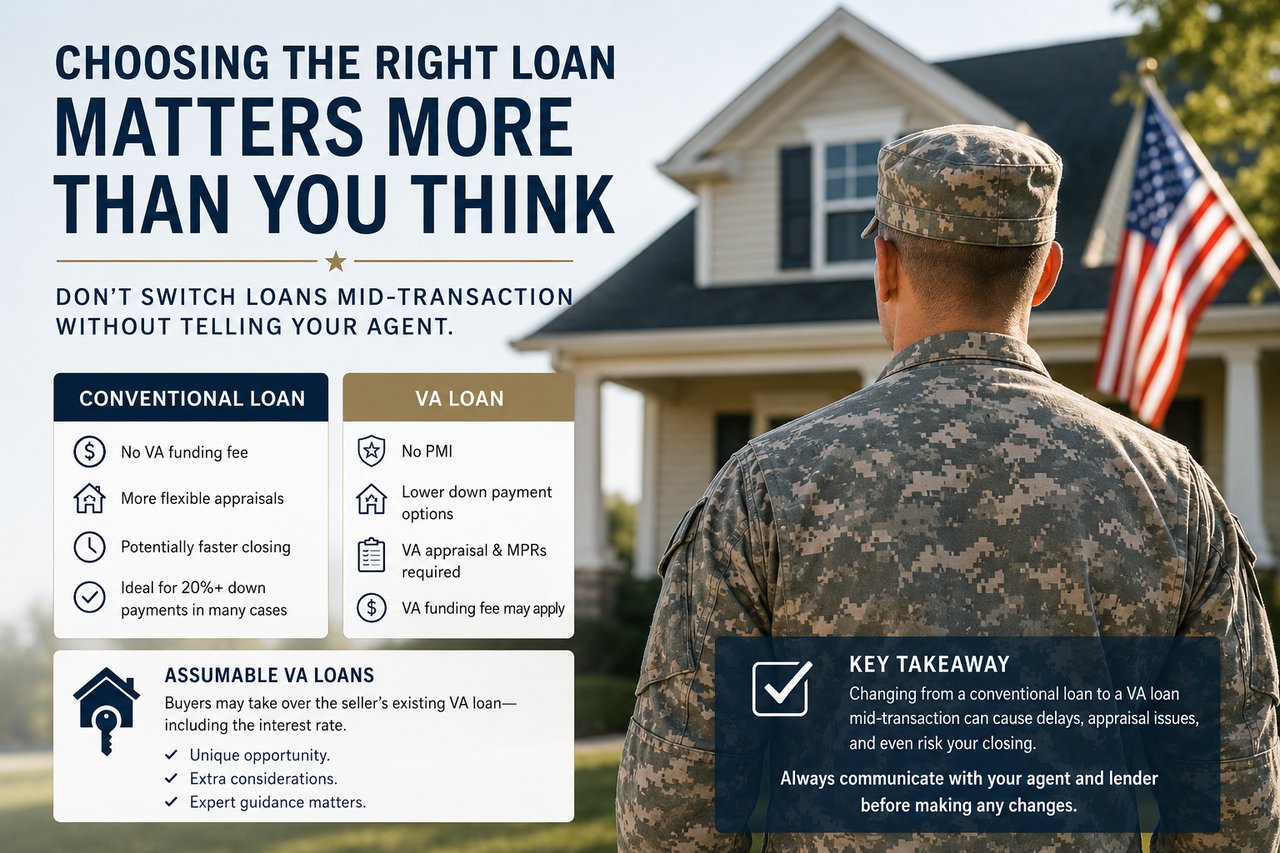

For many buyers—especially veterans and active-duty military members—a VA loan can be an incredible benefit. Lower down payment requirements, no private mortgage insurance (PMI), and competitive interest rates make VA financing attractive. But one mistake I occasionally see in real estate transactions is buyers changing loan products midstream—from a conventional loan to a VA loan—without immediately informing their real estate agent.

That seemingly small financing change can create major issues with timelines, appraisals, negotiations, and even whether a transaction closes at all.

If you're buying a home in Bluffton, Hilton Head, or anywhere in the Lowcountry, here's what you need to know before making that switch.

Why Changing Loan Types During a Transaction Matters

When an offer is submitted, the financing type is usually disclosed in the contract. Sellers evaluate offers differently based on:

- Loan program

- Down payment amount

- Closing timeline

- Appraisal requirements

- Perceived risk of financing delays

If your offer was accepted using conventional financing, then later changes to a VA loan, the transaction assumptions shift.

Potential impacts include:

1. New Appraisal Requirements

VA loans require a VA appraisal, which differs from conventional appraisals.

The VA appraisal evaluates:

- Market value

- Minimum Property Requirements (MPRs)

- Safety issues

- Habitability concerns

Things that may trigger repairs under VA financing:

- Peeling paint

- Damaged roofs

- Missing handrails

- Certain pest issues

- Broken windows

- Health or safety concerns

A home that qualifies under conventional financing may require repairs under VA standards.

That can reopen negotiations—or derail the transaction entirely.

2. Delays in Closing Timelines

Changing loan programs often means:

- New underwriting review

- Updated disclosures

- Additional documentation

- Potential appraisal delays

If your seller is coordinating another purchase or relocation, delays can create serious ripple effects.

3. Contract Compliance Issues

Some contracts specify financing terms.

Changing loan types without notifying your agent may create problems because:

- The seller may need to approve changes

- Contract amendments may be required

- Financing contingencies could be impacted

Transparency protects everyone involved.

Why VA Loans Aren't Always the Best Option—Especially with 20%+ Down

Many buyers assume: "I’m eligible for a VA loan, therefore it’s automatically the best choice."

Not necessarily.

When making 20% or more down, a conventional loan may sometimes be more financially advantageous.

Factors to compare:

VA Funding Fee

Most VA loans require a VA funding fee unless exempt.

For first-time VA use with no down payment, fees can exceed 2%.

Even with down payments, funding fees still apply in many cases.

Example:

$1,000,000 purchase price

20% down = $800,000 financed

A funding fee added to the loan could significantly increase borrowing costs.

(Some veterans with service-connected disability ratings are exempt.)

Conventional Loans May Offer:

✔ No VA funding fee

✔ Greater appraisal flexibility

✔ Potentially faster closing timelines

✔ More favorable terms for high-credit borrowers with large down payments

The "best" loan depends on:

- Credit profile

- Down payment

- Interest rates

- Long-term plans

- Tax strategy

- Seller requirements

Your lender should run multiple scenarios—not simply default to VA because eligibility exists.

Understanding Assumable VA Loans (And Why They Matter Right Now)

One major advantage unique to VA loans is assumability.

An assumable VA loan allows a qualified buyer to take over the seller's existing mortgage, including the interest rate.

This became extremely valuable as mortgage rates increased.

Example:

Seller has:

- 2.5% VA mortgage rate

- Remaining balance: $600,000

Buyers may assume that loan instead of obtaining today's higher-rate mortgage.

Potential savings can be substantial.

But Assumable VA Loans Have Challenges:

Buyers Need Cash for Equity Difference

If:

Home value = $900,000

Existing VA loan = $600,000

Buyer may need:

$300,000 cash (or secondary financing)

This limits the buyer pool.

Assumption Approval Takes Time

Loan assumptions require lender approval and often take significantly longer than traditional financing.

VA Entitlement Can Remain Tied Up

This is an often-overlooked issue.

If a non-veteran assumes a VA loan:

The original veteran seller's entitlement may remain partially tied to that loan until paid off.

That could affect future VA borrowing ability.

Veterans considering assumptions should discuss entitlement restoration with their lender before agreeing.

Why Communication With Your Realtor Matters

Your lender, agent, closing attorney, and seller all work within the same transaction ecosystem.

Changing financing—even if you think it improves your situation—should never happen in isolation.

Your agent needs to know because financing affects:

- Negotiation strategy

- Contract terms

- Appraisal expectations

- Repair discussions

- Timeline management

- Seller communication

The earlier changes are communicated, the easier problems are to solve.

Final Thoughts

VA loans remain one of the strongest home financing benefits available to eligible veterans and service members. But like any financial tool, they aren't automatically the best option in every scenario.

The right financing decision depends on your goals, cash position, timeline, and the specific property you're buying.

If you're purchasing a home in Bluffton, Hilton Head, Beaufort or the surrounding Lowcountry, understanding your financing options before making an offer can save significant stress—and potentially thousands of dollars.

Thinking about buying and unsure whether a VA or conventional loan makes more sense? Reach out—I'm happy to connect you with lenders who can compare scenarios and help you make an informed decision.